HFblogNews

Профессионал

Date: 2nd May 2024.

Market News – Stocks mixed; Yen support still on; Eyes on NFP & Apple tonight.

Economic Indicators & Central Banks:

Financial Markets Performance:

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stocks mixed; Yen support still on; Eyes on NFP & Apple tonight.

Economic Indicators & Central Banks:

- As the Fed maintained a “high-for-longer” stance, stocks gave up their gains with attention turning back to earnings.

- Chair Powell and the Fed were not as hawkish as feared and the markets reacted immediately and in textbook fashion to the still dovish policy stance.

- The Fed flagged that recent disappointing inflation readings could make rate cuts a while in coming, but Fed chief Jerome Powell characterized the risk of more hikes as “unlikely,” giving some solace to markets.

- Stocks traded mixed across Asia, while in Europe, DAX and FTSE futures are finding buyers and US futures are also in demand, after the Fed’s message.

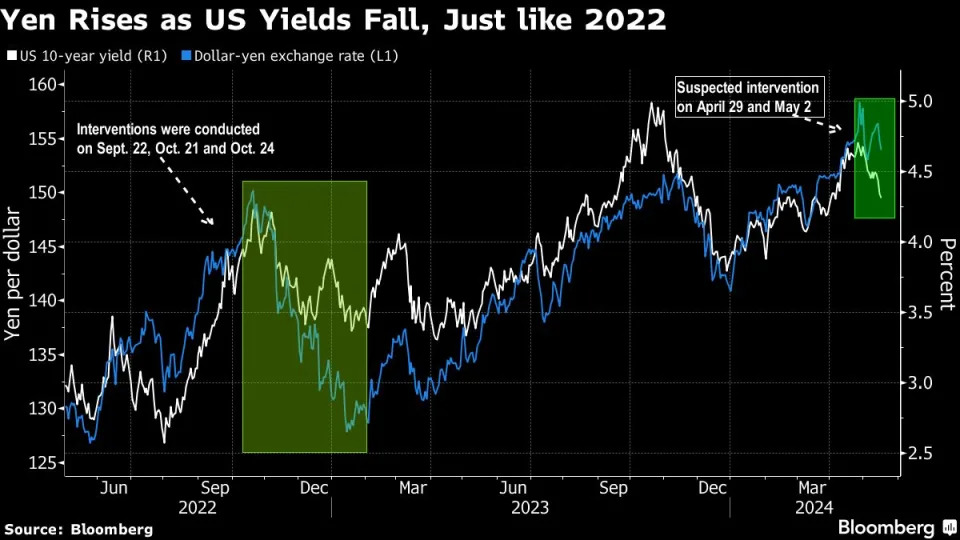

- Yen: Another suspected intervention by authorities, this time in late New York trading, ran into resistance from traders keen to keep selling the currency.

- Swiss CPI lifted to 1.4% y/y in April from 1.0% y/y in the previous month. Headline numbers are still at low levels and base effects play a role, with the different timing of Easter this year also likely to distort the picture. That said, the numbers may not question the SNB’s decision to cut rates, but they do not support another rate cut in June.

Financial Markets Performance:

- The USDIndex has corrected to 105.58, but USDJPY is already inching higher again, after a sharp drop to a low of 153.04 on Tuesday that sparked fresh intervention speculation. The pair is currently trading at 155.38.

- Treasury yields plunged and were down over double digits before profit taking set in.

- USOIL finished with a -3.6% loss to $79.00, the lowest since March 12. Currently it is as $79.53.

- Gold was up 1.4% to $2319.55 per ounce, reclaiming the $2300 level.

- Wall Street climbed initially with gains of 1.4% on the NASDAQ, 1.2% on the Dow, and 0.96% on the S&P500. The NASDAQ and S&P500 closed with losses of -0.3%, while the Dow was 0.23% firmer.

- The Hang Seng rallied more than 2%, and the ASX also posting slight gains, while CSI 300 and Nikkei declined.

- Apple’s earnings report is due after the US market closes today, will give investors a better sense of how the iPhone maker is weathering a sales slump, due in part to a sluggish China market.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Реклама: 🔥 Хочешь получить Telegram Premium и стать гуру Polymarket? Кликай сюда!