HFblogNews

Профессионал

Date: 3rd June 2024.

OPEC+ Announces Gradually Higher Supply and NVIDIA a New Accelerator.

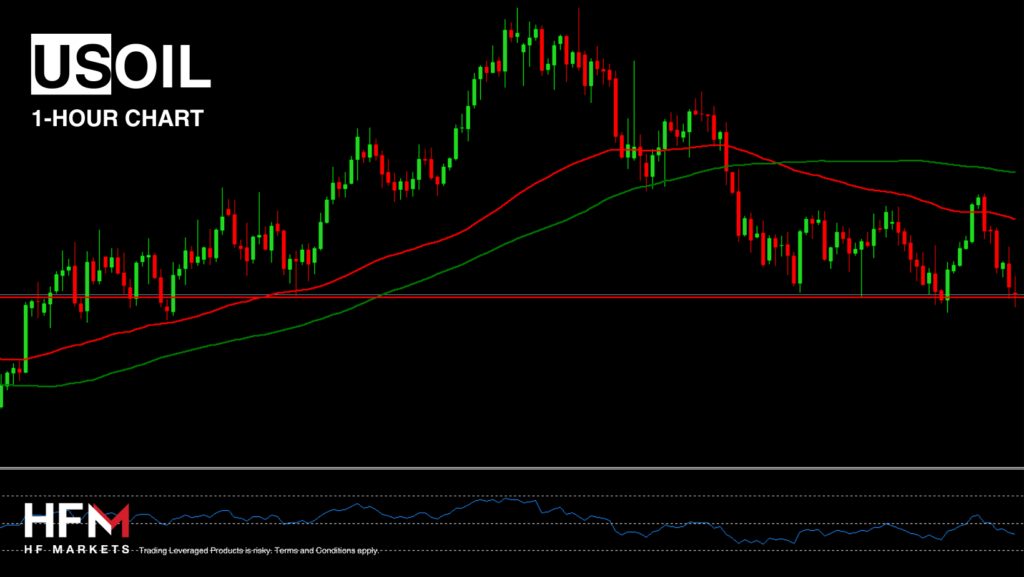

The price of Crude Oil fell almost 4.00% in the last 3 days of last week due to the OPEC+ meeting. The meeting is now at an end and journalists are pointing out 2 key points. The first, is that the OPEC+ group will keep limitations on production as it has since COVID-19. The second, is that countries which have voluntarily added additional cuts will have the option to reduce these cuts from September onwards.

According to analysts, the market should not necessarily “overreact”, because if OPEC+ increases supply, it will only be gradual. Additionally, analysts also advise the group will only look to re-introduce production if the market conditions allow it to. Nonetheless, traditionally, additional supply is known by analysts to apply downward pressure on commodities. This is something which can also be seen over the past week, but investors will be keen to see the price drop below the support level.

The support level has been a key psychological level for investors throughout the month of May, specifically on 3 occasions. The price is currently trading below the 50.00 on the RSI and below most longer-term Moving Averages. If the price declines below the 65.00 Fibonacci level at $76.70 per Barrel, momentum will signal possible further decline.

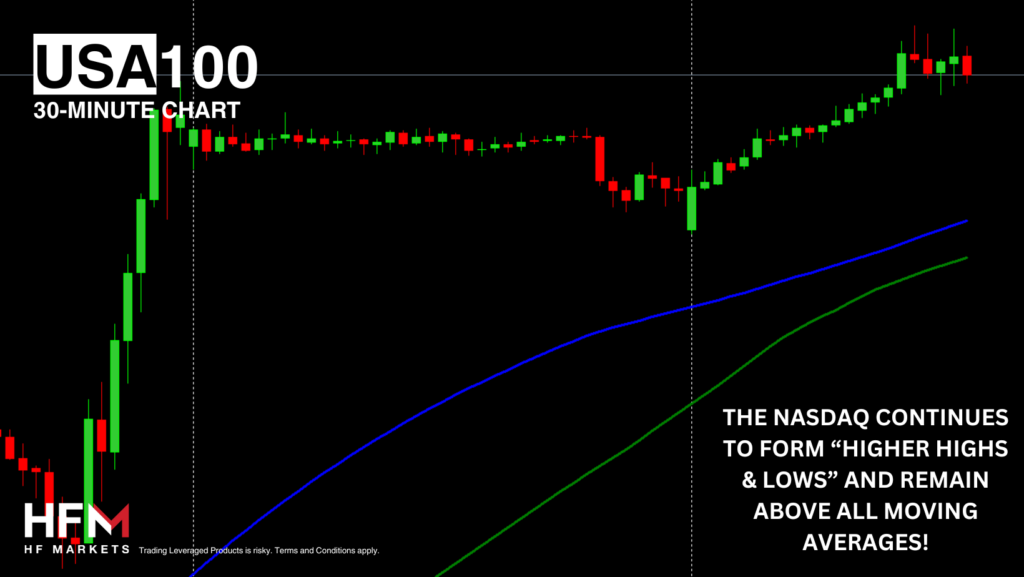

USA100 – NVIDIA Announces a New Accelerator Chip!

The NASDAQ struggled within the previous week and at one point was down more than 3.00%. However, a large surge of buyers towards the end of Friday’s session saw a strong rebound and the index also trades higher during today’s Asian session. The NASDAQ is currently being influenced by 3 factors. However, investors will also give importance to the pricing of rate adjustments after the US employment data.

The first factor prompting investors to increase tech-stock exposure is NVIDIA. The CEO of the company has again advised the technology and AI market will continue to grow and become more aggressive. In addition to this, Mr Huang advised NVIDIA is releasing a new accelerator chip and promises more within the upcoming year.

A second positive factor for not only the NASDAQ, but global indices, is most analysts believe the European Central Bank will lower interest rates for the first time in the current cycle. If more global banks decide to reduce the restrictiveness of their monetary policy, stocks will become more attractive. However, only if the move is not a response to potential economic contraction.

Lastly investors are also taking advantage of the lower entry point and feel an improved sentiment as Oil prices are declining. Investors hope lower oil prices will apply less upward pressure on inflation.

If the price rises above $18,638.83 the price will form a bullish breakout pattern which indicates upward movement. However, for a stronger and longer-term bullish trend, investors will be keen for the price to increase above the 75-Bar EMA and 100-Bar SMA. These two moving averages are currently priced at $18,658.28 and $18,733.30.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

OPEC+ Announces Gradually Higher Supply and NVIDIA a New Accelerator.

- Oil declines as the European Cash Open edges closer. Oil prices have fallen for 4 consecutive days measuring almost 4.00%.

- OPEC+ members advise the group will have the option to not continue voluntary cuts from September onwards.

- All US and global indices start Monday’s trading higher after a poor end to May 2024. The bullish price gap illustrates a potential “risk-on” market.

- NVIDIA announces its next generation of accelerator chips and promises annual upgrades. NVIDIA stocks are already trading 0.55% higher in pre-trading hours.

The price of Crude Oil fell almost 4.00% in the last 3 days of last week due to the OPEC+ meeting. The meeting is now at an end and journalists are pointing out 2 key points. The first, is that the OPEC+ group will keep limitations on production as it has since COVID-19. The second, is that countries which have voluntarily added additional cuts will have the option to reduce these cuts from September onwards.

According to analysts, the market should not necessarily “overreact”, because if OPEC+ increases supply, it will only be gradual. Additionally, analysts also advise the group will only look to re-introduce production if the market conditions allow it to. Nonetheless, traditionally, additional supply is known by analysts to apply downward pressure on commodities. This is something which can also be seen over the past week, but investors will be keen to see the price drop below the support level.

The support level has been a key psychological level for investors throughout the month of May, specifically on 3 occasions. The price is currently trading below the 50.00 on the RSI and below most longer-term Moving Averages. If the price declines below the 65.00 Fibonacci level at $76.70 per Barrel, momentum will signal possible further decline.

USA100 – NVIDIA Announces a New Accelerator Chip!

The NASDAQ struggled within the previous week and at one point was down more than 3.00%. However, a large surge of buyers towards the end of Friday’s session saw a strong rebound and the index also trades higher during today’s Asian session. The NASDAQ is currently being influenced by 3 factors. However, investors will also give importance to the pricing of rate adjustments after the US employment data.

The first factor prompting investors to increase tech-stock exposure is NVIDIA. The CEO of the company has again advised the technology and AI market will continue to grow and become more aggressive. In addition to this, Mr Huang advised NVIDIA is releasing a new accelerator chip and promises more within the upcoming year.

A second positive factor for not only the NASDAQ, but global indices, is most analysts believe the European Central Bank will lower interest rates for the first time in the current cycle. If more global banks decide to reduce the restrictiveness of their monetary policy, stocks will become more attractive. However, only if the move is not a response to potential economic contraction.

Lastly investors are also taking advantage of the lower entry point and feel an improved sentiment as Oil prices are declining. Investors hope lower oil prices will apply less upward pressure on inflation.

If the price rises above $18,638.83 the price will form a bullish breakout pattern which indicates upward movement. However, for a stronger and longer-term bullish trend, investors will be keen for the price to increase above the 75-Bar EMA and 100-Bar SMA. These two moving averages are currently priced at $18,658.28 and $18,733.30.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Реклама: 🔥 Хочешь получить Telegram Premium и стать гуру Polymarket? Кликай сюда!