HFblogNews

Профессионал

Date: 13th August 2024.

The Pound Rises, But Cracks Emerge in the UK Employment Sector.

The Great British Pound is increasing in value against the US Dollar and also against all other currencies. However, the economic data coming out of the UK this morning paints a very different picture. Therefore, many investors question whether the Pound will indeed maintain bullish momentum.

The number of individuals claiming unemployment benefits from 135,000 within a single month, the highest since the first COVID lockdown. The six-month average for the UK Claimant Count Change (number of unemployment benefits) is 22,233. Therefore, 135,000 added within a single month is a concern for investors and the Bank of England.

In addition to this, the UK Average Earnings Index fell from 5.7% to 4.5% which is lower than expectations. The fall is likely to apply less upward pressure on inflation and can eventually prompt the Bank of England to consider an earlier rate cut. However, the positive from the morning’s UK data is the unemployment rate. The UK unemployment rate fell from 4.4% to 4.2%, a 4-month low.

It is vital for investors to continue monitoring the GBP index, which is currently trading 0.23% higher. However, if data continues to disappoint throughout the week, the traditional react would lead to a weakening of the British Pound. If individual wish to speculate a depreciating GBP, investors also have the option to trade the GBPNZD which has been the best performing currency of the past week.

Regarding the GBPUSD exchange rate, the price will also largely be dependant on this afternoon’s Producer Price Index. As the US session edges closer, investors will turn their attention to the PPI, which analysts expect to fall to 2.3%. If the Producer Price Index reads higher than expectations, the US Dollar may increase in value while the market’s risk appetite declines. As a result, the Pound can quickly give up gains from the past 24 hours.

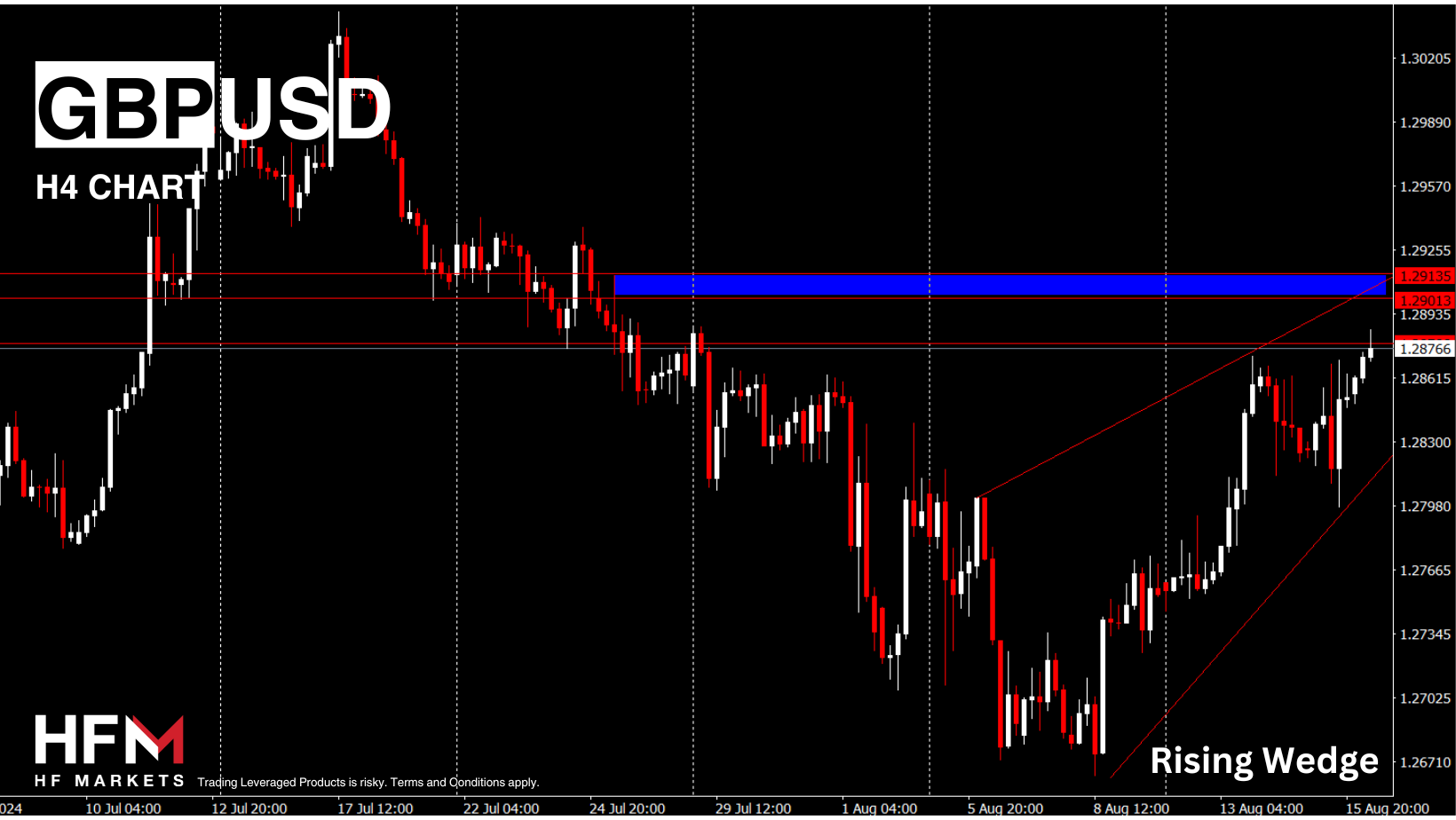

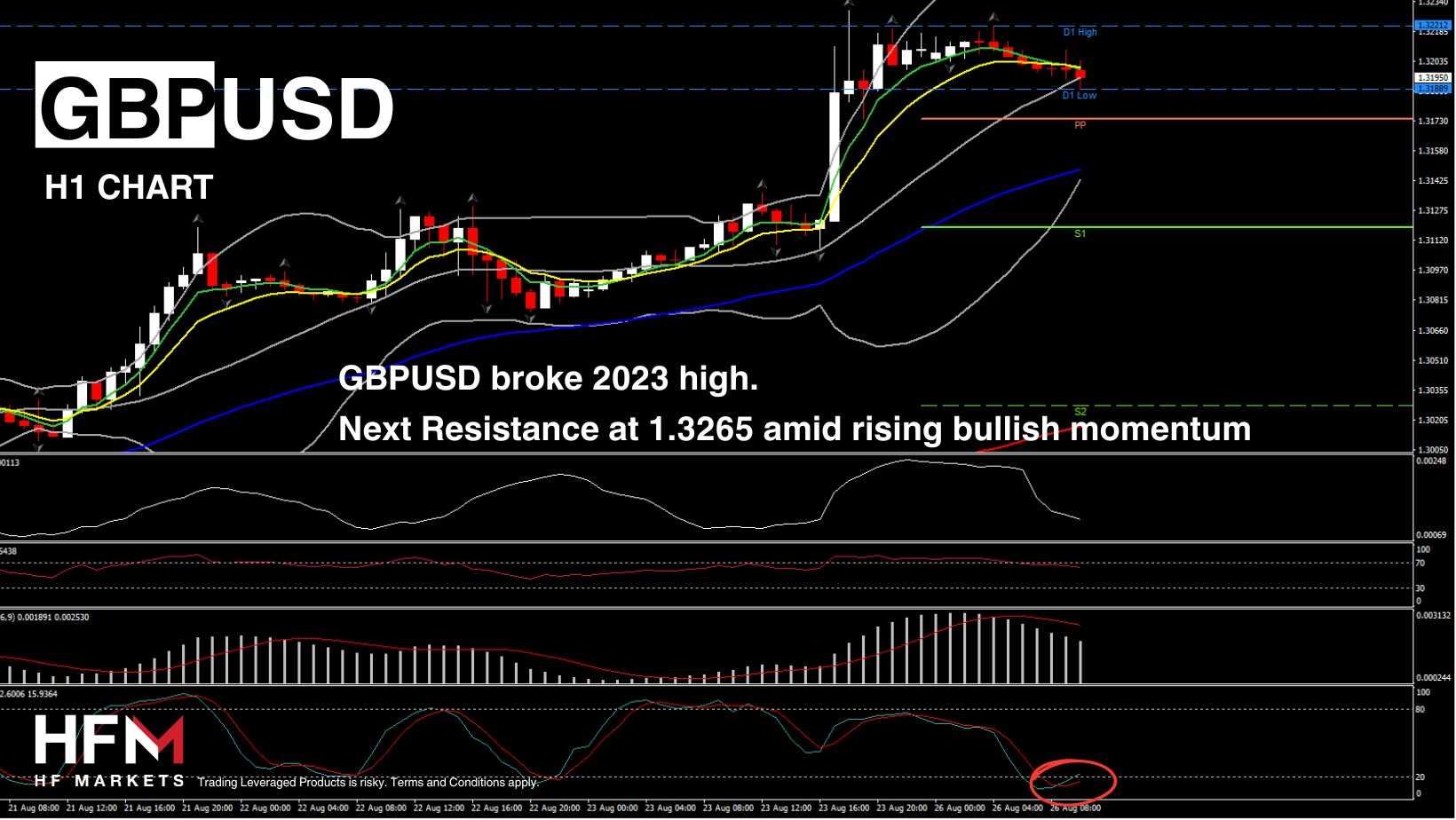

Currently, the price of the GBPUSD is trading above most moving averages, oscillators and the VWAP indicating potential upward price movement. However, as mentioned above, the price movement will be dependant on the upcoming economic releases. If the price trades above 1.28037 and 1.28092, the exchange rate may rise in value in the short term. However, ideally the US PPI will need to read lower than expectations as the breakout takes place.

USA30 – Investors On Edge Ahead Of Inflation And Home Depot’s Earnings Report!

The Dow Jones continues to honour the price pattern of the previous 2 trading sessions as per yesterday’s analysis. However, this is now likely to change as Home Depot will release their earnings report in the upcoming hours. Additionally, this afternoon’s Producer Price Index will be a key price driver. Shareholders will be hoping for a lower-than-expected PPI.

Home Depot has beat their earnings expectations over the past 4 quarters, but investors will also be looking for guidance for the upcoming quarters. Investors expect Earnings Per Share to rise from $3.63 to $4.55 and for revenue to rise by $6 billion. If the company beat expectations the stock potentially can rise and support the Dow Jones. Over the past 12 months the stock has risen 4.80% and has a dividend yield of 2.60%.

During this morning’s Asian session, the VIX is trading more than 2.00% lower which is positive for the Dow Jones. Investors will continue to monitor the VIX and US Bond Yields. If both decline, the price movement is likely to improve. Throughout the Asian session the Dow Jones has risen 0.32% and is attempting to move back to the resistance level. However, positive data is required to breakout of this level and form a possible bullish trend.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The Pound Rises, But Cracks Emerge in the UK Employment Sector.

- The Pound increases in value, but UK employment data signals economic stagnation and weakening employment.

- The UK number of individuals claiming unemployment benefits rises 135,000, the highest in over 4 years.

- The Dow Jones trades sideways but this may change as Home Depot is due to release their earnings report.

- Investors turn their attention to the US Producer Inflation Rate which analysts expect to fall to 2.3%.

The Great British Pound is increasing in value against the US Dollar and also against all other currencies. However, the economic data coming out of the UK this morning paints a very different picture. Therefore, many investors question whether the Pound will indeed maintain bullish momentum.

The number of individuals claiming unemployment benefits from 135,000 within a single month, the highest since the first COVID lockdown. The six-month average for the UK Claimant Count Change (number of unemployment benefits) is 22,233. Therefore, 135,000 added within a single month is a concern for investors and the Bank of England.

In addition to this, the UK Average Earnings Index fell from 5.7% to 4.5% which is lower than expectations. The fall is likely to apply less upward pressure on inflation and can eventually prompt the Bank of England to consider an earlier rate cut. However, the positive from the morning’s UK data is the unemployment rate. The UK unemployment rate fell from 4.4% to 4.2%, a 4-month low.

It is vital for investors to continue monitoring the GBP index, which is currently trading 0.23% higher. However, if data continues to disappoint throughout the week, the traditional react would lead to a weakening of the British Pound. If individual wish to speculate a depreciating GBP, investors also have the option to trade the GBPNZD which has been the best performing currency of the past week.

Regarding the GBPUSD exchange rate, the price will also largely be dependant on this afternoon’s Producer Price Index. As the US session edges closer, investors will turn their attention to the PPI, which analysts expect to fall to 2.3%. If the Producer Price Index reads higher than expectations, the US Dollar may increase in value while the market’s risk appetite declines. As a result, the Pound can quickly give up gains from the past 24 hours.

Currently, the price of the GBPUSD is trading above most moving averages, oscillators and the VWAP indicating potential upward price movement. However, as mentioned above, the price movement will be dependant on the upcoming economic releases. If the price trades above 1.28037 and 1.28092, the exchange rate may rise in value in the short term. However, ideally the US PPI will need to read lower than expectations as the breakout takes place.

USA30 – Investors On Edge Ahead Of Inflation And Home Depot’s Earnings Report!

The Dow Jones continues to honour the price pattern of the previous 2 trading sessions as per yesterday’s analysis. However, this is now likely to change as Home Depot will release their earnings report in the upcoming hours. Additionally, this afternoon’s Producer Price Index will be a key price driver. Shareholders will be hoping for a lower-than-expected PPI.

Home Depot has beat their earnings expectations over the past 4 quarters, but investors will also be looking for guidance for the upcoming quarters. Investors expect Earnings Per Share to rise from $3.63 to $4.55 and for revenue to rise by $6 billion. If the company beat expectations the stock potentially can rise and support the Dow Jones. Over the past 12 months the stock has risen 4.80% and has a dividend yield of 2.60%.

During this morning’s Asian session, the VIX is trading more than 2.00% lower which is positive for the Dow Jones. Investors will continue to monitor the VIX and US Bond Yields. If both decline, the price movement is likely to improve. Throughout the Asian session the Dow Jones has risen 0.32% and is attempting to move back to the resistance level. However, positive data is required to breakout of this level and form a possible bullish trend.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Реклама: 🔥 Хочешь получить Telegram Premium и стать гуру Polymarket? Кликай сюда!