HFblogNews

Профессионал

Date : 25th January 2023.

Market Update – January 25 – Asian markets return to hot AUD & NZD Inflation.

Many Asian markets back (China & Taiwan remain closed all week) and higher today, NYSE suffered tech meltdown (250+ stocks paused trading on Open) US Stocks mixed following a raft of uninspiring Earnings. #MSFT had its weakest quarterly sales growth in 6-yrs but EPS beat. -0.22% on the day & -1.02% after hours. PMI data from EZ & US weak, but better than expected, UK data weak & missed. USDIndex recovered 102.00, EUR close to 9-mth highs. Hot CPI (8.4% & 32-yr high vs 7.6%) in AUD on bid & it lifts the outlook for hikes from RBA 7/2. AUD over 0.7100 close to 6-mth highs, NZD CPI also hotter than expected. Gold $1930, USOIL holds $80.00, BTC $22.7k.

Biggest FX Mover @ (07:30 GMT) AUDNZD (+1.21%). Rallied from 1.0800 yesterday to trade at 1.0960 now. MAs aligned higher, MACD histogram & signal line positive & rising. RSI 85.12, OB & stalling, H1 ATR 0.00205, Daily ATR 0.0070.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

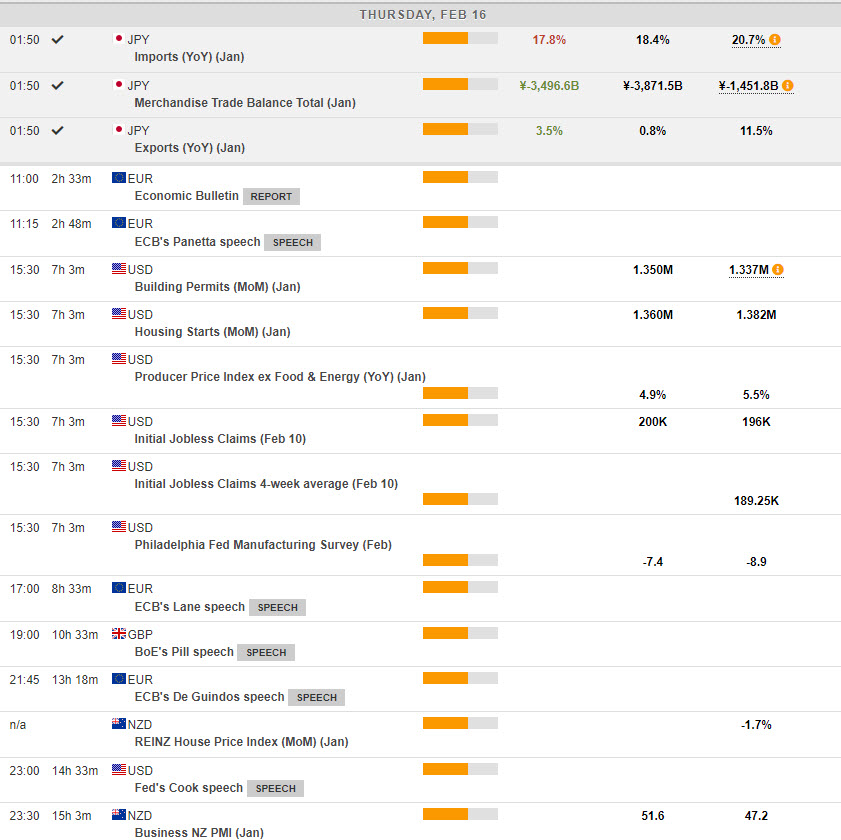

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – January 25 – Asian markets return to hot AUD & NZD Inflation.

Many Asian markets back (China & Taiwan remain closed all week) and higher today, NYSE suffered tech meltdown (250+ stocks paused trading on Open) US Stocks mixed following a raft of uninspiring Earnings. #MSFT had its weakest quarterly sales growth in 6-yrs but EPS beat. -0.22% on the day & -1.02% after hours. PMI data from EZ & US weak, but better than expected, UK data weak & missed. USDIndex recovered 102.00, EUR close to 9-mth highs. Hot CPI (8.4% & 32-yr high vs 7.6%) in AUD on bid & it lifts the outlook for hikes from RBA 7/2. AUD over 0.7100 close to 6-mth highs, NZD CPI also hotter than expected. Gold $1930, USOIL holds $80.00, BTC $22.7k.

- The USD Index rallied to 102.20, on Tuesday, before PMI & Earnings weighed and it trades at 101.60 today.

- EUR – holds over 1.0900 now, having tested below 1.0845 yesterday, following a new 9-mth high at 1.0925 on Monday.

- JPY – Hit resistance at 131.00 and support at 130.00 yesterday, back to 130.40 now.

- GBP – Sterling hit 1.2260 and 5-day lows following the weak PMI data, a revision of ONS data that showed UK to be the 2nd slowest growing of the G7 nations and record Government borrowing in December. (

- Stocks – The US markets traded very mixed yesterday amid concerns over Earnings (-0.27% to +0.96%). US500 -0.07%, (-2.86) 4016 band holds the key 4000 level US500 FUTS trade at 4019. #MSFT had its weakest Q4 sales growth in 6-yrs but EPS beat, stock fell -0.22% on the day & -1.02% after hours.

- USOil – topped at $82.58 on Monday and declined to test before inventories data showed a build of 8.4 million barrels (vs. an expected drawdown of 2.4 million barrels) and prices rallied to $81.50 and holds at $81.00 now.

- Gold – has hit 9-mth highs today at $1935 again today and trades at $1930 now. The spectre of CB’s reluctant to talk pivot and season factors help the key commodity.

- BTC – Continues to hold the $20k handle this week and is back to test $21k today.

Biggest FX Mover @ (07:30 GMT) AUDNZD (+1.21%). Rallied from 1.0800 yesterday to trade at 1.0960 now. MAs aligned higher, MACD histogram & signal line positive & rising. RSI 85.12, OB & stalling, H1 ATR 0.00205, Daily ATR 0.0070.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Реклама: 🔥 Хочешь получить Telegram Premium и стать гуру Polymarket? Кликай сюда!