HFblogNews

Профессионал

Date: 5th October 2023.

Market Update – October 5 – Markets try to take a breather, oil slumps.

Rebounding from some pivotal, psychological levels, the vast majority of world equity indices rose yesterday, helped by a decrease in yields. Buying in the US intensified in the last minutes of trading led by large-cap techs such as TSLA (+5.93%), MSFT & AMZN. US500 was up 0.8%, its largest rise in 3 weeks and US100 settled +1.5% at the end of the day. As mentioned above, after reaching a high of 4.88% during the Asian session, the 10Y benchmark was lower later in the day, ending the day almost 15 bps lower. Part of this was due to the rather worse-than-expected ADP jobs data, which helped consolidate expectations of a further Fed pause in November (now at 80%). One aspect that the financial media are somewhat glossing over as they are concentrating on the gigantic -46% drawdown on the long end of the US curve – is the great steepening of the 2y-10y, now at 32bps (it was -1% at the end of July). Also on the US side, while we anxiously await tomorrow’s NFP data, it should be noted that today marks the end of the suspension of student debt payments decreed after Covid which will probably weigh heavily on many households. In Europe and the UK, better-than-expected composite PMI data helped the respective currencies to do well, while the USDIndex is also near overbought levels.

The big mover of the day was Oil, with crude very heavy (-5.6%) on the day of the OPEC+ JMMC, characterised first by Russia and Saudi Arabia’s apparent willingness to continue with production cuts, then by Novak’s (Russia) statements that ”OPEC+ may tweak its decisions if needed… as we see a record-high global oil demand”.

Today: highlights include GE Trade Balance, US Jobless Claims, Fed’s Mester, Barkin, Daly, ECB’s Lane & de Guindos.

Interesting Mover: USOil ($83.50) has lost its 3m long uptrend, is below its 50MA and testing a strong support level at the $83.50 area, with RSI (14) at 39.72.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 5 – Markets try to take a breather, oil slumps.

Rebounding from some pivotal, psychological levels, the vast majority of world equity indices rose yesterday, helped by a decrease in yields. Buying in the US intensified in the last minutes of trading led by large-cap techs such as TSLA (+5.93%), MSFT & AMZN. US500 was up 0.8%, its largest rise in 3 weeks and US100 settled +1.5% at the end of the day. As mentioned above, after reaching a high of 4.88% during the Asian session, the 10Y benchmark was lower later in the day, ending the day almost 15 bps lower. Part of this was due to the rather worse-than-expected ADP jobs data, which helped consolidate expectations of a further Fed pause in November (now at 80%). One aspect that the financial media are somewhat glossing over as they are concentrating on the gigantic -46% drawdown on the long end of the US curve – is the great steepening of the 2y-10y, now at 32bps (it was -1% at the end of July). Also on the US side, while we anxiously await tomorrow’s NFP data, it should be noted that today marks the end of the suspension of student debt payments decreed after Covid which will probably weigh heavily on many households. In Europe and the UK, better-than-expected composite PMI data helped the respective currencies to do well, while the USDIndex is also near overbought levels.

The big mover of the day was Oil, with crude very heavy (-5.6%) on the day of the OPEC+ JMMC, characterised first by Russia and Saudi Arabia’s apparent willingness to continue with production cuts, then by Novak’s (Russia) statements that ”OPEC+ may tweak its decisions if needed… as we see a record-high global oil demand”.

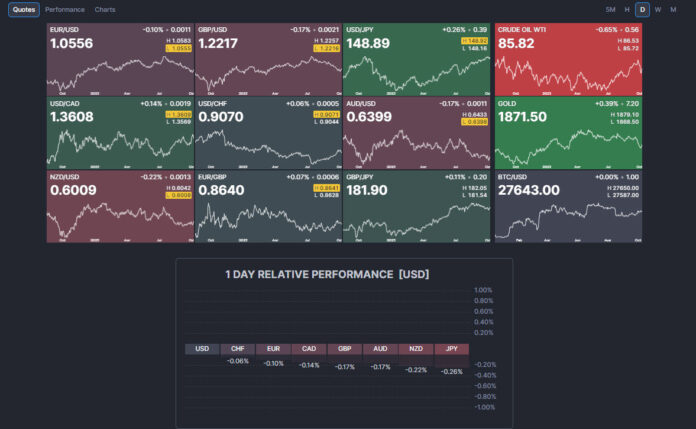

- FX – USDIndex -0.09% @ 106.43; GBPUSD & EURUSD flat today (1.2137/1.0506) after rising +0.5% & +0.36% respectively yesterday, USDJPY 148.78, USDCAD is -0.06% @ 1.3736 after rising approx. 2.65% since 20/09. Swiss Franc is strengthening, USDCHF-0.08% @ 0.9165.

- Stocks – US and EU futures fractionally negative this morning, -0.1% and -0.2% on average respectively. Yesterday TSLA +5.93%, MSFT +1.78%, GOOGL +2.23% AMZN +1.83%.

- Commodities – USOil rebounded this morning +0.44% at $84.79, UKOil +0.52% @ $86.40.

- Metals – Gold flat @ $1821.47, XAGUSD +0.57% @ 21.12.

Today: highlights include GE Trade Balance, US Jobless Claims, Fed’s Mester, Barkin, Daly, ECB’s Lane & de Guindos.

Interesting Mover: USOil ($83.50) has lost its 3m long uptrend, is below its 50MA and testing a strong support level at the $83.50 area, with RSI (14) at 39.72.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Реклама: 🔥 Хочешь получить Telegram Premium и стать гуру Polymarket? Кликай сюда!